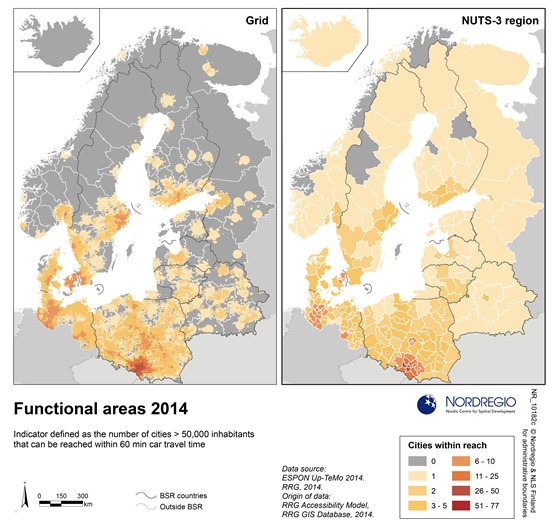

59 Maps

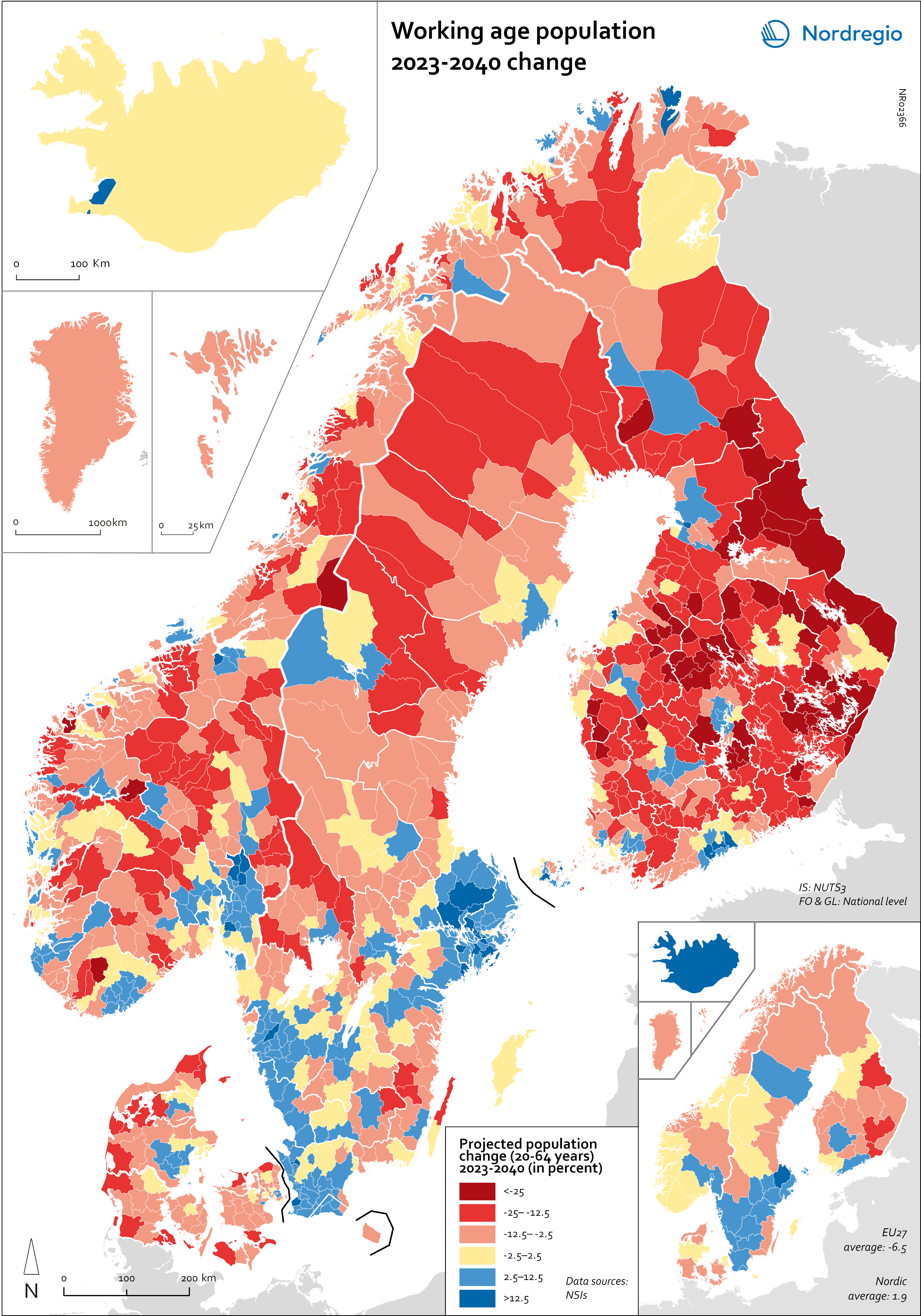

Working age population – 2023-2040 change

This map illustrates the projected change in the working-age population across Nordic municipalities (large map) and regions (small map) from 2023 to 2040. The working-age population is defined here as individuals aged 20 to 64. The blue areas on the maps represent municipalities and regions where the working-age population is expected to increase during this period. In contrast, the red areas indicate a projected decline in the working-age population. These projections are based on data from Nordic statistical institutes, though it’s important to note that the underlying assumptions may vary between Nordic countries. In most of the Western world, the working-age population is decreasing. In the EU, this age group is expected to decrease by 6.5% between 2023 and 2040. Only five EU countries – Malta, Luxembourg, Ireland, Sweden and Belgium – are expected to enjoy growth in the working-age population during this period. However, in the Nordic Region as a whole, the working-age population is expected to grow slightly, with an average increase of 1.9%. As the map shows, the distribution is quite varied, with considerable differences both between and within the countries. The biggest increase is expected in Iceland (28%), followed by Sweden (5.8%), Åland (3.9%) and Norway (0.6%). Decreases are expected in Finland (-0.5%), the Faroe Islands (-2.6%), Denmark (-3.2%) and Greenland (-11.4%). This development is in addition to the decreases already experienced by Finland since 2013. In general, the trend of growing populations in cities and decreasing populations in rural areas is expected to continue. The regions that are expected to have the highest working-age population growth include Höfuðborgarsvæðið in Iceland, Uppsala (+13%), Stockholm (+12%), Skåne (+9%), Halland (+7%) and Västra Götaland (+6%) in Sweden, Uusimaa (+8%) and Pirkanmaa (+5%) in Finland, and Oslo and Viken in Norway (+5%). In addition, Copenhagen municipality (+5%), Rødovre (+9%)…

2025 April

2025 April - Demography

- Labour force

- Nordic Region

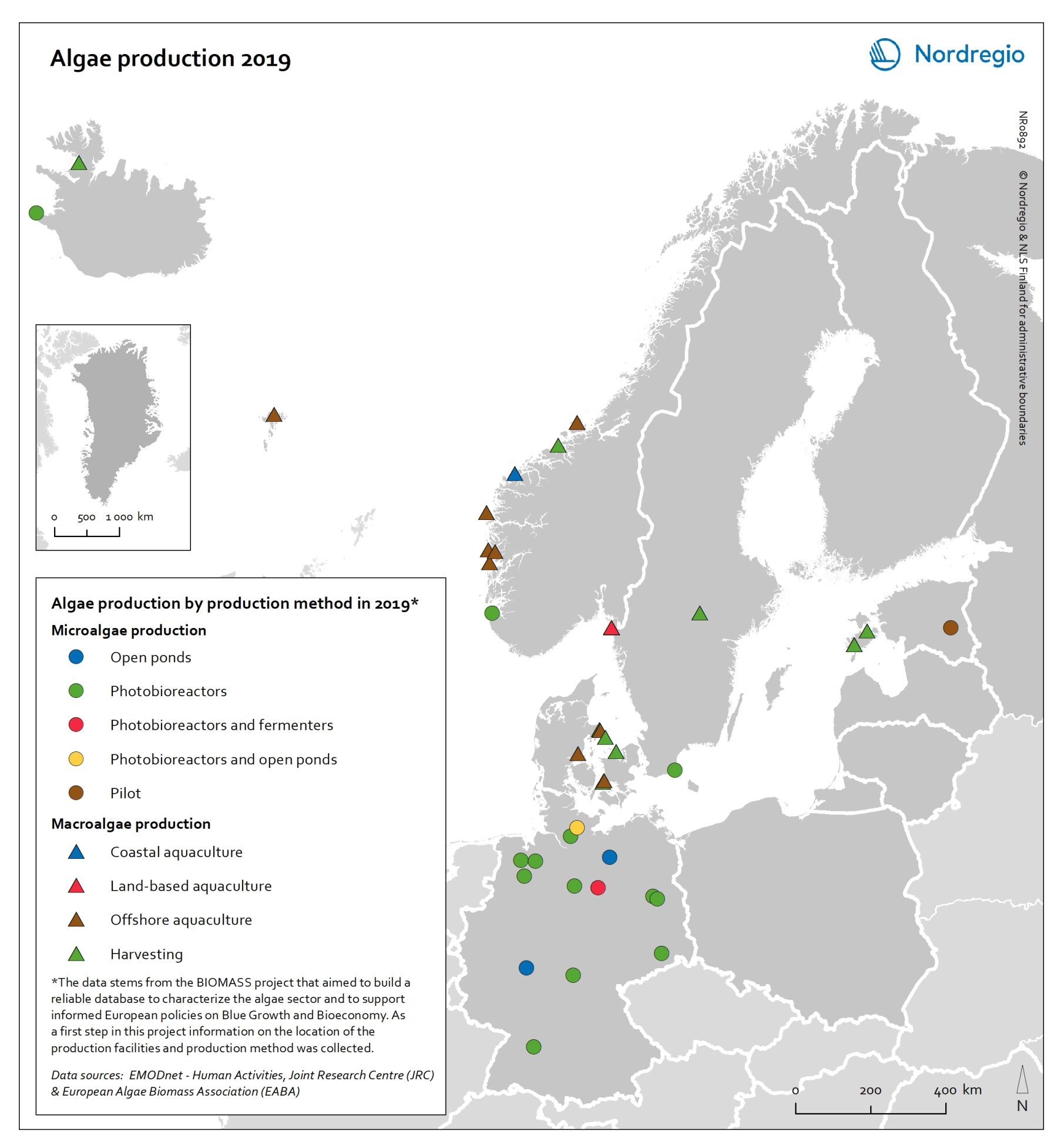

Algae production in 2019

This map shows location of algae production by production method in the Nordic Arctic and Baltic Sea Region in 2019 Algae and seaweeds are gaining attention as useful inputs for industries as diverse as energy and human food production. Aquatic vegetation – both in the seas and in freshwater – can grow at several times the pace of terrestrial plants, and the high natural oil content of some algae makes them ideal for producing a variety of products, from cosmetic oils to biofuels. At the same time, algae farming has added value in potential synergies with farming on land, as algae farms utilise nutrient run-off and reduce eutrophication. In addition, aquatic vegetation is a highly versatile feedstock. Algae and seaweed thrive in challenging and varied conditions and can be transformed into products ranging from fuel, feeds, fertiliser, and chemicals, to third-generation sugar and biomass. These benefits are the basis for seaweed and algae emerging as one of the most important bioeconomy trends in the Nordic Arctic and Baltic Sea region. The production of algae for food and industrial uses has hence significant potential, particularly in terms of environmental impact, but it is still at an early stage. The production of algae (both micro- and macroalgae) can take numerous forms, as shown by this map. At least nine different production methods were identified in the region covered in this analysis. A total of 41 production sites were operating in Denmark, Estonia, the Faroe Islands, Iceland, Norway, Germany, and Sweden. Germany has by far the most sites for microalgae production, whereas Denmark and Norway have the most macroalgae sites.

- 2021 December

- Arctic

- Baltic Sea Region

- Nordic Region

- Others

Change in share of biofuels in transport from 2010 to 2018

This map shows change in share of biofuels in final energy consumption in transport in the Nordic Arctic and Baltic Sea Region from 2010 to 2018. Even though a target for greater use of biofuels has been EU policy since the Renewable Energy and Fuel Quality Directives of 2009, development has been slow. The darker shades of blue on the map represent higher increase, and the lighter shades of blue reflect lower increase. The lilac color represent decrease. The Baltic Sea represents a divide in the region, with countries to the north and west experiencing growth in the use of biofuels for transport in recent years. Sweden stands out (16 per cent growth), while the other Nordic countries has experienced more modest increase. In the southern and eastern parts of the region, the use of biofuels for transport has largely stagnated. Total biofuel consumption for transport has risen more than the figure indicates due to an increase in transport use over the period.

- 2021 December

- Arctic

- Baltic Sea Region

- Nordic Region

- Transport

Share of biofuels in transport in 2018

This map shows the share of biofuels in final energy consumption in transport in the Nordic Arctic and Baltic Sea Region in 2018. There has been considerable political support for biofuels and in the EU, this debate has been driven by the aim of reducing dependency on imported fuels. For instance, 10 per cent of transport fuel should be produced from renewable sources. The darker shades on the map represent higher proportions, and the lighter shades reflect lower proportions. As presented by the map, only Sweden (20.7%) had reached the 10 per cent target in the Nordic Arctic and Baltic Region in 2018. Both Finland (8.3%) and Norway (8.3%) were close by the target, while the other countries in the region were still lagging behind, particularly the Baltic countries.

- 2021 December

- Arctic

- Baltic Sea Region

- Nordic Region

- Transport

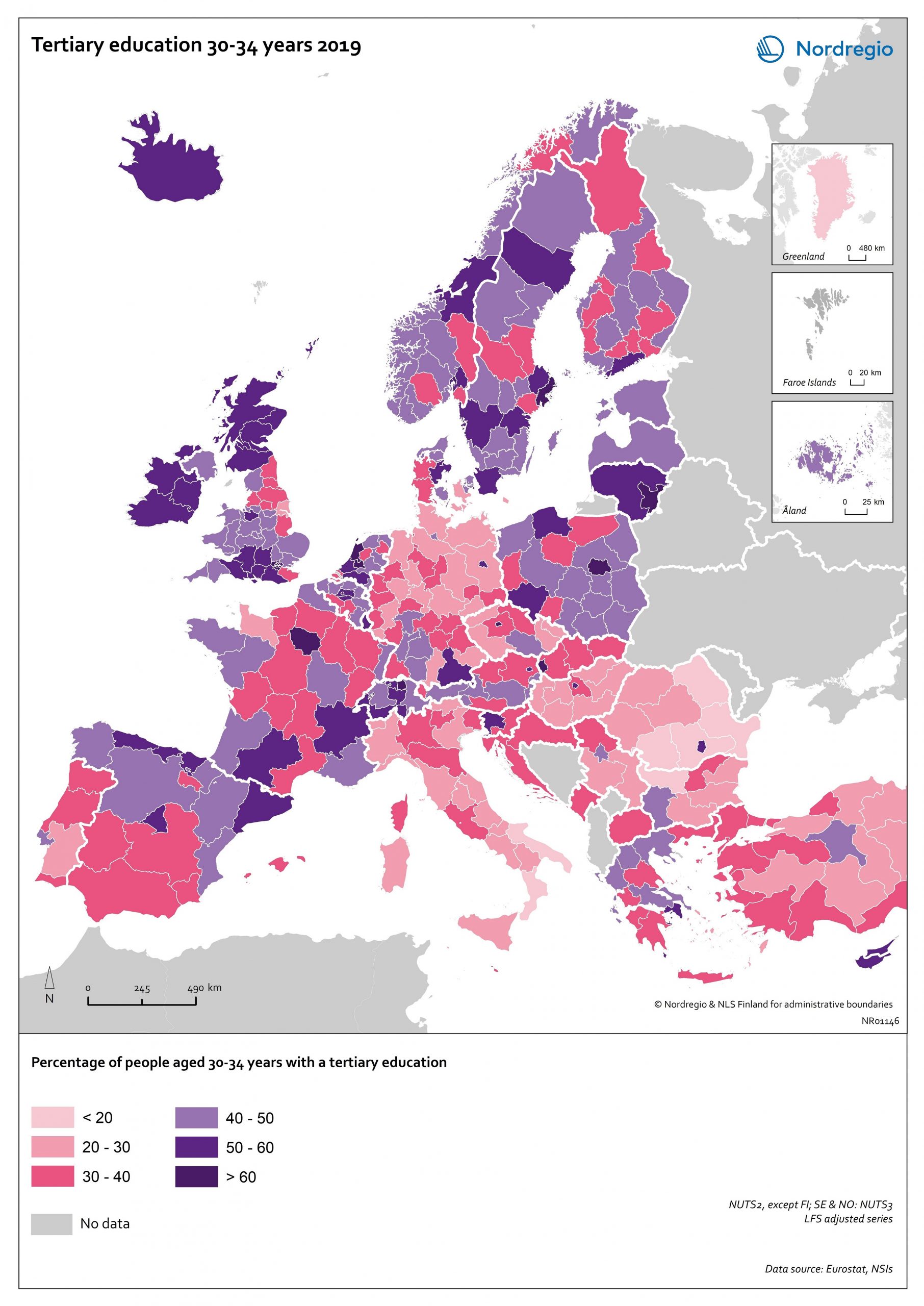

Tertiary education attainment level of 30- to 34-year-olds 2019

The map shows the proportion of the population aged 30-34 years old, who had a tertiary education at the European level in 2019. Purple shades indicate higher proportions, and pinkish shades reflect lower proportions. It is common to show the education attainment for the age group 30-34 since it is an age group where most people have finalised their studies. The focus on this age group makes it easier to see recent trends and outcomes of policies. Overall, over 40% of Europeans aged 30-34 years old had a tertiary education in 2019. Young people in the Nordic countries are among the most educated, with approximately half of 30 to 34-year-olds achieving a tertiary education across all Nordic countries. The highest proportions can be found in the capital regions. Stockholm is particularly noteworthy, with over 60% of 30 to 34-year-olds having had a tertiary education. Regions with prominent universities also stand out – for example, Skåne, Uppsala, Västerbotten and Västra Götaland (Sweden), Trøndelag (Norway) and Østjylland (Denmark).

- 2020 October

- Baltic Sea Region

- Demography

- Europe

- Nordic Region

- Others

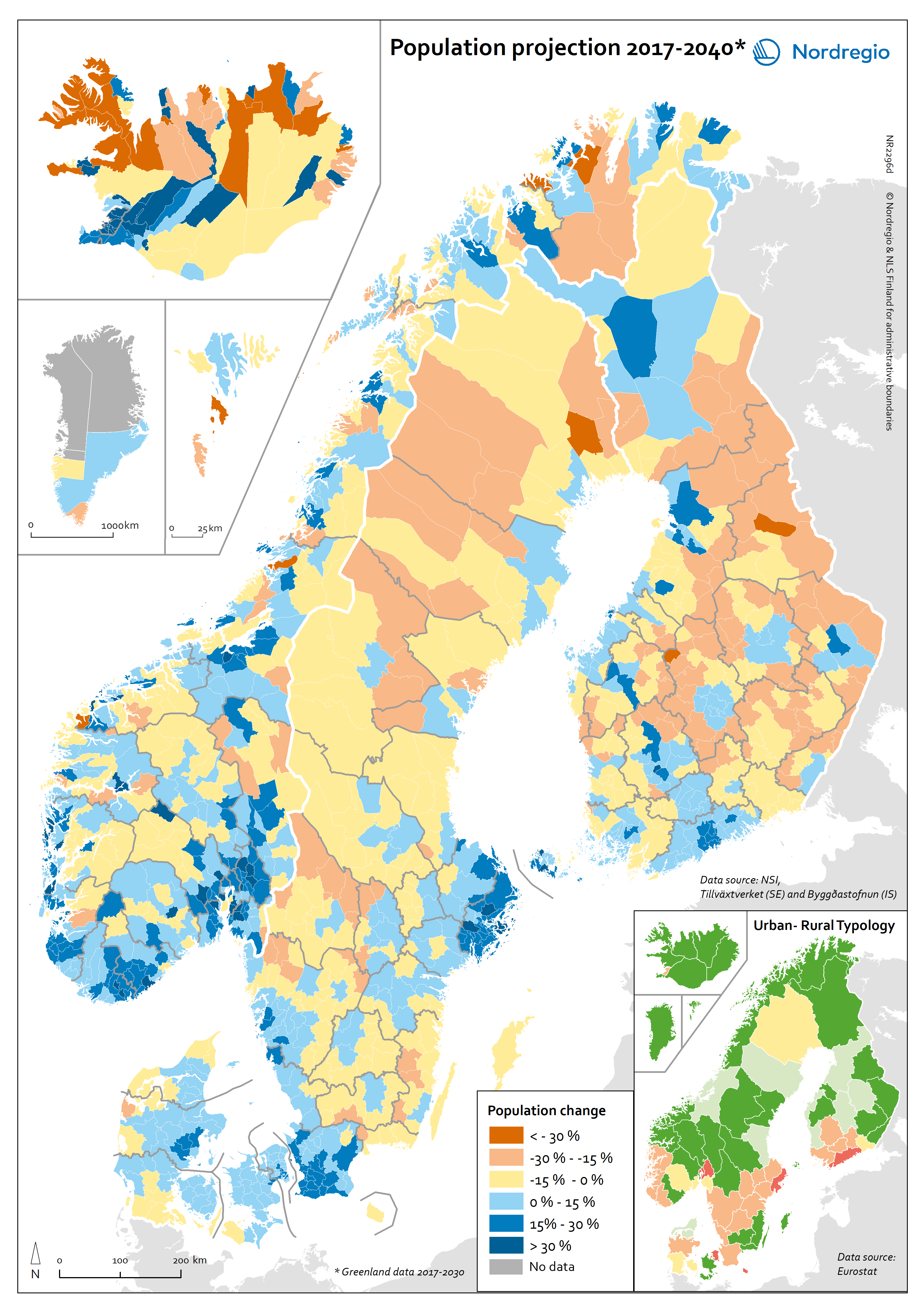

Population projection 2017-2040

This map shows the expected population change in Nordic municipalities by looking at the change between 2017 and 2040. The colours on the main map indicates the percentage of population change at municipal level between 2017 and 2040. Shades of red indicate a population decline, whereas shades of blue indicate a population increase. The colours on the regional map (bottom-right corner) indicates the type of region according to the Eurostat’s urban-rural typology (see: http://nordregio.org/maps/urban-rural-typology-of-nordic-regions/): shades of red indicate predominantly urban regions, yellow for intermediate regions and shades of green for predominantly rural regions. In the two types of regions classified as predominantly rural (“light green” and „dark green“ regions), population growth largely remains concentrated in larger towns and their suburbs. This is particularly the case in Sweden and Finland. For instance, the regional capitals Östersund in Jämtland (SE) and Seinäjoki in South Ostrobothnia (FI) are expected to have larger populations in 2040 than today, while most other municipalities in these regions will decline. In Norway and Iceland, a somewhat more nuanced pattern applies. Here population growth is not only expected in regional capitals and other larger towns, but also in some smaller and more remote municipalities. In Denmark, finally, population growth is expected for large parts of the country until 2040, in more rural and urban areas alike. Population loss is only expected in some of the most remote municipalities at the Northern, Eastern and Southern borders of the country. While the population loss in rural regions is hence expected to continue across the Nordic Region, it appears to be more pronounced in some countries than in others. In the predominantly urban (“red”) regions, the opposite pattern applies: With very few exceptions, municipalities in these regions are expected to experience a growth in population numbers until 2040.

- 2020 September

- Demography

- Nordic Region

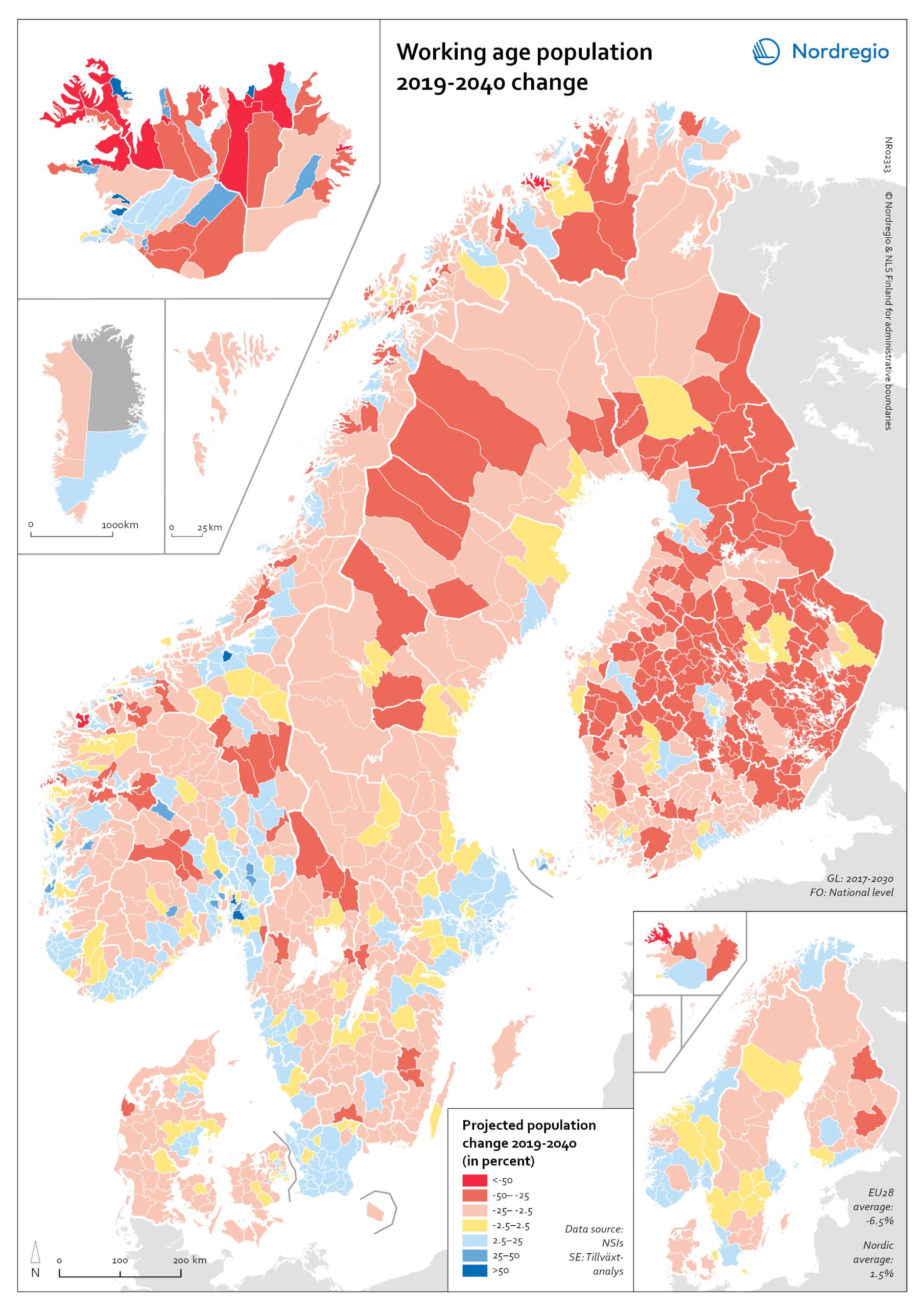

Change in working age population 2019-2040

This map shows the projected working age population change at municipal level during the period 2019-2040 While the total population of the Nordic Region is projected to grow by 8% to 29.5 million by 2040, the growth of the working-age population (15–64 years) is expected to be more modest at 1.5%. The working-age population also referred to as the potential labour supply, refers to all people in the population aged 15–64 years. It is a potential supply because it includes all those who fit the age requirement, despite some not actually being available for the labour market (e.g. full-time students, those with long-term illnesses or disabilities that affect their ability to work). The potential labour supply at the local level is constantly shifting due to trends such as ageing, migration and urbanisation. The red areas on the map indicate a projected working-age population decline and blue areas an increase. The yellow areas indicate a stable development. On a national level Greenland (-16.2%), the Faroe Islands (-6.6%), Finland (-3%) and Denmark (-2%) are projected to see a decrease in the working-age population, while increases are projected in Sweden (4%), Norway (4.6%), Åland (9.1%) and Iceland (10.9%). It is worth noting that, even in the parts of the Nordic Region where the working-age population is expected to shrink, the projections are less severe than the EU28 average (-6.5%). Greenland and Faroe Islands are the only exceptions. At the municipal level, the variation is even more striking with the majority (72%) of Nordic municipalities projected to experience a decrease in the size of the working-age population. As Figure 6.2 shows, this trend is most pronounced in Finland (decline of the working-age population in 90% of the municipalities) and Denmark (81%) and less apparent in Sweden (67%), Iceland (64%) and Norway (61%). Most of…

- 2020 February

- Demography

- Labour force

- Migration

- Nordic Region

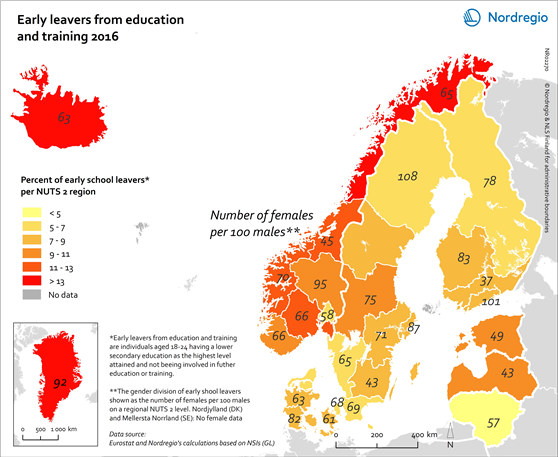

Early leavers from education and training 2016

This map shows the percent of early school leavers in the Nordic Region (NUTS 2 level) and Baltic states in 2016, calculated as the total number of individuals aged 18-24 having a lower secondary education as the highest level attained and not being involved in further education or training. The numbers in each region indicate the proportion of females per 100 males. The yellow/red shading indicates the percent of early school leavers in 2016. The lighter the colour the lower the percentage of early school leavers in 2016. The grey colour indicates no data. Early school leaving is of concern in the Nordic Region to varying degrees. From a pan-European perspective, the Danish (7.2%), Swedish (7.4%) and Finnish (7.9%) averages all fall below the EU average (10.7%) and are in line with the Europe 2020 target of below 10%. The Norwegian average (10.9%) remains slightly above the target but is comparable to the EU average. The average rate of early school leaving in Iceland (19.8%) is substantially higher than the other Nordic countries and the EU average. There is both a spatial and a gender dimension to this problem. The spatial dimension of early school leaving is highlighted in this map, which shows rates of early school leaving in the Nordic Region at the NUTS 2 level. The map highlights the comparatively high rates in Norway, particularly in the north. It is worth noting that, although still high in a Nordic comparative perspective, early school leaving rates have decreased in all Norwegian regions since 2012. Rates are also high in Greenland, with a staggering 57.5% of young people aged 18–24 years who are not currently studying and who have lower secondary as their highest level of educational attainment. The map also shows the gender dimension of early school leaving, with…

- 2018 February

- Baltic Sea Region

- Labour force

- Nordic Region

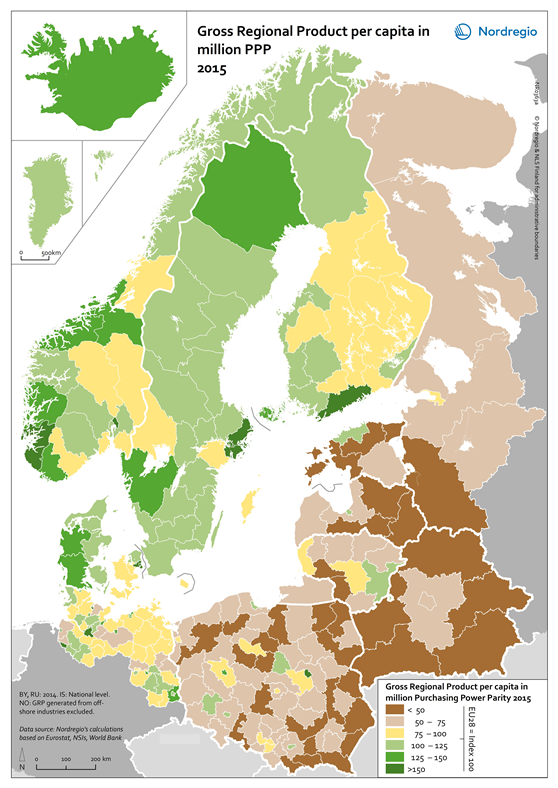

Gross Regional Product per capita in million PPP 2015

This map shows the gross regional product per capita in million purchasing power parity (PPP) in all Nordic and Baltic Regions in 2015. The green tones indicate regions with a gross regional product per capita above the EU28 average. The darker the tone the higher the gross regional product per capita. The brown/yellow shading indicates regions with a gross regional product per capita below the EU28 average. The darker the tone the lower the gross regional product per capita. In economic development terms, the Nordic Region continues to perform well in relation to the EU average. Urban and capital city regions still show high levels of GDP per capita reflecting the established pattern throughout Europe. Stockholm, Oslo, Helsinki, Copenhagen and the western Norwegian regions are among the wealthiest in Europe, again confirming that the capital regions and larger cities are the strongest economic centres in the Nordic Region. In addition to these urban regions, some others also display high levels of GRP per capita. What is interesting is that in the aftermath of the economic crisis some second-tier city regions, such as Västra Götaland with Gothenburg in Sweden, are now also displaying fast growth rates as indeed are some less metropolitan regions in the western part of Denmark. These regions display GRP per capita levels which correspond to, or even exceed, those of most metropolitan regions in Europe. most of the central and eastern parts of Finland remain below the EU average.

- 2018 February

- Baltic Sea Region

- Economy

NEET rate for young people 18-25 years in 2016

Share of young people aged 18-25 years neither in employment nor in education and training in 2016 There are a range of reasons why a young person may become part of the “NEETs” group, including (but not limited to): complex personal or family related issues; young people’s greater vulnerability in the labour market during times of economic crisis; and the growing trend towards precarious forms of employment for young people. Successful reengagement of these young people with learning and/or the labour market is a key challenge for policy makers and is vital to reducing the risk of long-term unemployment and social exclusion later in life. The map highlights two Polish regions, Podkarpackie and Warminsko-Mazurskie, as having the highest NEET rates in the BSR. High rates can also be found in several other Polish regions as well as the Northern and Eastern Finland Region. The lowest NEET rates in the Baltic Sea Region can be found in the Norwegian Capital Region, followed by several regions in Sweden, Norway and Denmark.

- 2017 June

- Baltic Sea Region

- Labour force

Youth unemployment rate in 2016

The map highlights two Polish regions, Podkarpackie and Lubuskie, as having the highest youth unemployment rates in the BSR. Several other regions in Poland, along with regions in Northern Finland, Central Sweden and the southernmost Swedish region of Skåne, have also been rather severely hit by youth unemployment. The lowest youth unemployment rates can be found in several Russian regions, among them St. Petersburg, and in regions in Northern Germany and Northern Norway.

- 2017 June

- Baltic Sea Region

- Labour force

- Nordic Region

Tertiary education among working-age population, change 2010-2015

The Nordic countries, as well as Estonia and Lithuania, have had among the highest levels of tertiary education in Europe in recent years. This map demonstrates that many regions, particularly those in Poland, are catching up. Several Lithuanian and Latvian regions have also had high rates of positive change between 2010 and 2015. The most modest growth rates, between 0 and 1.5 percent change, were experienced in two Estonian regions, one in Denmark and one in Northern Germany. Mecklenburg-Vorpommern and Brandenburg, in North-Eastern Germany, were the only regions within the Baltic Sea Region to experience a decrease in the share of working-age persons with tertiary level education from 2010-2015.

- 2017 March

- Baltic Sea Region

- Labour force

- Nordic Region